Free Cash Flow Under the Microscope

From the article

Evidence from 238 non-GAAP cash flow metrics and 562 reconciling adjustments reveals where S&P 500 companies diverge in their free cash flow presentations. Free cash flow (FCF) is one of the most closely watched non-GAAP metrics, particularly as investors focus on the enormous capital spending required for AI infrastructure. Yet FCF is not defined under GAAP, and companies do not necessarily calculate it the same way. SEC C&DIs observe that free cash flow is “typically calculated” as GAAP cash flows from operating activities less capital expenditures. But what does “typically” mean in practice? How closely do companies follow that formula? What do they include in capital expenditures, and how often do they make additional adjustments? To answer those questions, I examined free cash flow reconciliations furnished on Form 8-K under Item 2.02 by S&P 500 companies between January and March 2026. The final sample includes 205 companies, or slightly more than 40% of the S&P 500 population, reporting 238 non-GAAP cash flow-related metrics. Across those reconciliations, I identified 562 individual adjustments used to bridge GAAP cash flows from operating activities to the reported non-GAAP measure. Most Companies Keep FCF Simple The traditional formula remains dominant. More than half of the 238 metrics contain only one reconciling adjustment between the starting GAAP measure and the ending non-GAAP measure. In most cases, that adjustment is related to capital expenditures. However, the terminology varies. Companies use labels such as “Capital expenditures,” “Purchases of property, plant, and equipment,” and “Additions to property, plant, and equipment.” These adjustments generally represent economically similar concepts of investment in long-term assets and were grouped into a broad capital expenditures category for this analysis. But similar does not mean identical. Some companies include capitalized software, lease-related items, or other expenditures within their capital spending measures, while others present those items separately — or do not incorporate them at all. Thus, even apparently simple FCF calculations may capture somewhat different cash outflows. The Adjustments Go Well Beyond CAPEX The chart below describes the most common adjustments used to calculate free cash flow metrics. Source: SEC filings, analysis by Deep Quarry. Capital expenditure-related items account for 255 adjustments, or about 45% of all reconciling items identified. For purposes of this analysis, the category broadly includes capital expenditures, purchases and additions of property, plant, and equipment, proceeds from asset dispositions, and capitalized software-related items. Yet more than half of all adjustments fall outside that broad category. Changes in working capital account for 45 adjustments, followed by M&A-related items (30), restructuring (27), tax-related adjustments (24), and litigation-related items (19). Other adjustments involve investments, noncontrolling interests, dividends and distributions, interest, and debt-related items. These findings highlight the central comparability problem. Free cash flow may have a familiar cash from operations starting point, but companies can incorporate very different cash flows into the final metric. The absence of a GAAP definition gives issuers substantial flexibility, and identically or similarly labeled measures do not necessarily capture the same economics. FCF Usually Moves Down, Not Up Free cash flow also differs from the pattern commonly associated with non-GAAP earnings. Recent Calcbench research found that 89% of S&P 500 companies reporting non-GAAP earnings presented a measure exceeding the corresponding GAAP result. FCF moves in the opposite direction. In this sample, 217 of 238 cash flow-related non-GAAP metrics, or about 91%, were lower than the corresponding GAAP measure, typically cash flows from operating activities. The reason is straightforward: capital expenditures generally reduce operating cash flow when calculating FCF. Positive company-specific adjustments are not uncommon. Companies may exclude restructuring payments, acquisition-related cash flows, litigation settlements, tax items, or other costs. But in most cases, those positive adjustments only partially offset capital expenditure deductions, leaving reported FCF below operating cash flow. The broader takeaway is that free cash flow is not a standardized metric, and there is a variation in how companies calculate it. While most FCF calculations remain anchored in the traditional operating cash flow-less-CAPEX framework, there are differences in what counts as capital expenditures, which additional adjustments are made, and which economically significant obligations remain outside the metric. These variations can materially affect FCF comparison across issuers. This is an abridged version of the analysis. The full post , available to Deep Quarry subscribers, provides more insight into how FCF metrics are calculated and gives specific examples. The underlying company-level dataset, including 238 reconciled metrics and the classification of 562 individual adjustments, is available to Deep Quarry premium subscribers upon request. Investment, Tax and Legal Disclaimer: This article is for informational purposes only and does not constitute investment, tax or legal advice. The content contained herein is not to be relied upon as the basis for any investment or other decision. Nothing herein should be construed as a solicitation, recommendation, endorsement, or offer to buy or sell any particular security, product, or service. The author has not taken into account the specific investment objectives, financial situation, or particular needs of any specific person who may read this material. Investing involves inherent risks, and there can be no guarantee that any investment or company mentioned will be suitable or profitable for any investor's investment portfolio. Readers are strongly advised to conduct their own thorough research and consult with a qualified and licensed financial professional and legal counsel before making any investment decisions. Past performance is not indicative of future results. Opinion Disclaimer: The opinions and views expressed in this article are those of the author and the parties quoted and not necessarily those of The National Law Review or its Guest Contributors.

Continue reading on The National Law ReviewYou might also wanna read

Gartner: CFOs Must Distinguish AI Deployment from Value Creation in Finance

Gartner warns CFOs that deploying AI in finance functions does not automatically equate to value creation. While 66% of organizations report

cpapracticeadvisor.com·1mo ago

cpapracticeadvisor.com·1mo agoGartner: CFOs Must Distinguish AI Deployment from Value Creation in Finance

Gartner warns CFOs that deploying AI in finance functions does not automatically equate to value creation. While 66% of organizations report

cpapracticeadvisor.com·1mo ago

Tech giants impose AI spending caps as pressure to demonstrate ROI intensifies

Major tech companies including Uber, Microsoft, and Meta are implementing cost-control measures like spending caps and dashboards to manage

qz.com·17d ago

qz.com·17d ago

Research on LLM Output Drift in Financial Workflows: Quantifying Consistency Across Model Sizes

This research paper examines the critical issue of output drift in Large Language Models (LLMs) deployed for financial workflows. The study

CFOs Funded the AI Revolution. Most Didn't Get One.

nexairi.com·29d ago

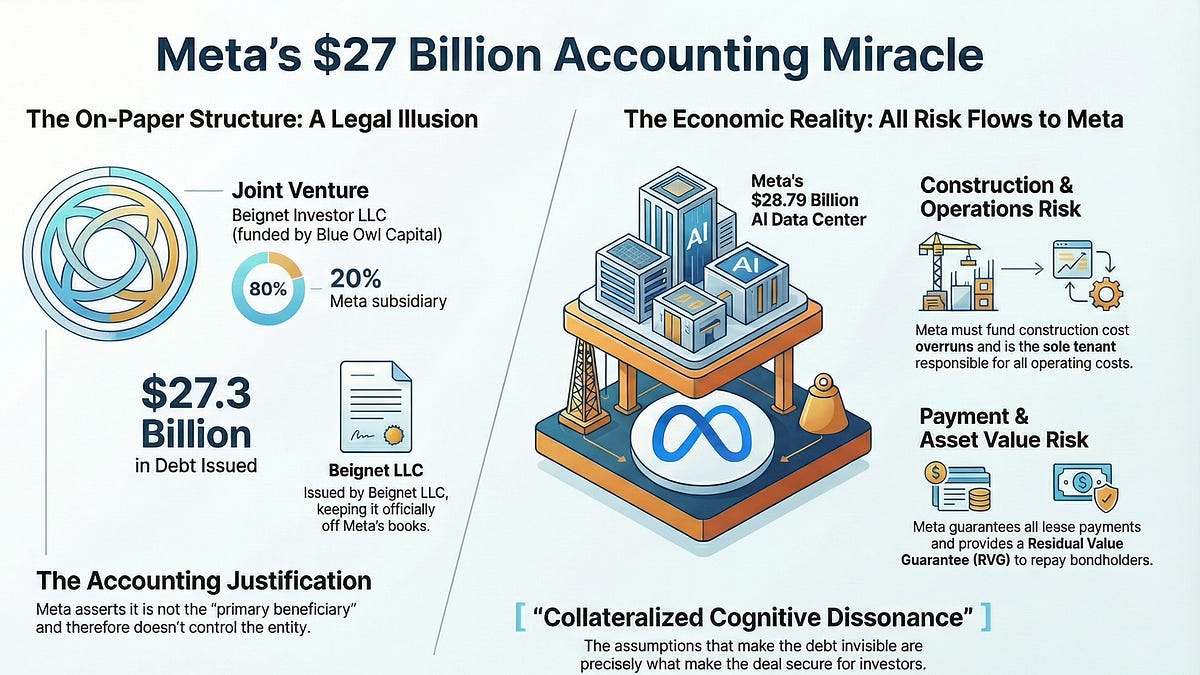

Analysis: Meta's $27 Billion Off-Balance Sheet Accounting Through Data Center Joint Venture

FSG LLC (Flexible Standards Group) assigns a preliminary A+ rating to Beignet Investor LLC's proposed $27.30 billion senior secured amortizi

stohl.substack.com·7mo ago

stohl.substack.com·7mo agoUS SEC preparing to scrap quarterly reporting requirement

reuters.com·3mo ago

Comments

Sign in to join the conversation.

No comments yet. Be the first.