Estimating the Term Structure of Corporate Bond Risk Premia

Source

libertystreeteconomics.newyorkfed.orgEstimating the Term Structure of Corporate Bond Risk Premianewyorkfed.org

libertystreeteconomics.newyorkfed.orgEstimating the Term Structure of Corporate Bond Risk Premianewyorkfed.orgYou might also wanna read

Market Reactions to AI Model Releases: Analysis of Bond Yield Movements

The article examines how transformative AI technologies affect financial markets, specifically analyzing US bond yield movements around majo

TLT ETF Analysis: 30-Year Treasury Yield as Key Indicator for Bond Rally Potential

TLT (iShares 20+ Year Treasury Bond ETF) is analyzed for its potential rally over the next 12 months. Despite 75 basis points of Federal Res

briefly.co·1mo ago

briefly.co·1mo ago

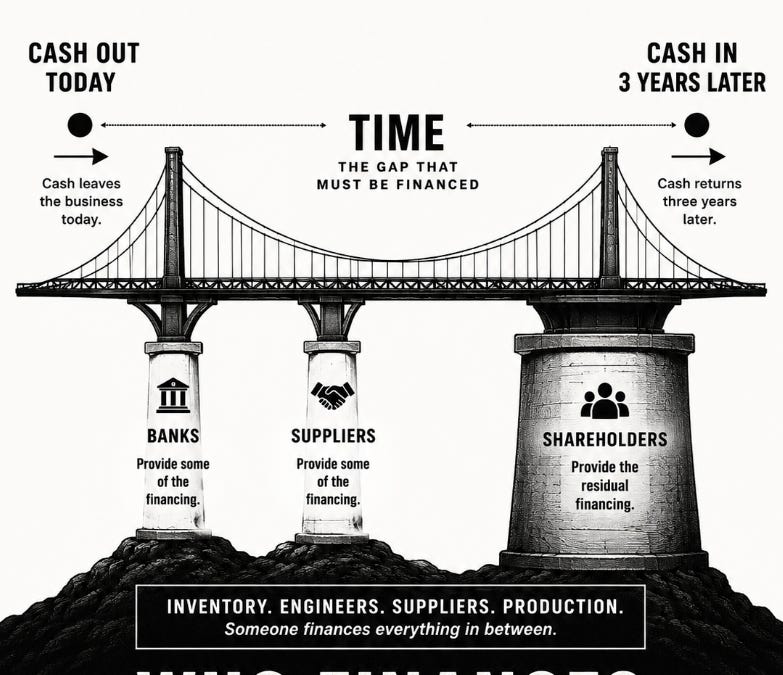

Balance-Sheet Duration: The Hidden Financing Risk in Deep-Science Manufacturing

This is a brief teaser for a paid article about balance-sheet duration risk in deep-science manufacturing. The core premise is that cash out

Hedge funds become essential players in the $1-trillion-a-day Treasury market

The article discusses the enormous scale of the U.S. Treasury market, where $1 trillion in securities trade daily and trillions more are use

econ.st·25d ago

econ.st·25d ago

Bond market inflation warning adds economic pressure on Trump ahead of midterm elections

The article reports that rising bond market interest rates are creating economic pressure on the Trump administration, with 10-year Treasury

chicagotribune.com·1mo ago

chicagotribune.com·1mo agoBond market inflation warning adds economic pressure on Trump ahead of midterm elections

The article reports that rising bond market interest rates are creating economic pressure on the Trump administration, with 10-year Treasury

chicagotribune.com·1mo ago

Comments

Sign in to join the conversation.

No comments yet. Be the first.